Before I even met my husband, I was all too familiar with the strain finances can put on even the healthiest of marriages. It’s easy to see how financial infidelity or even simple disagreements can cause discord within a family. All you have to do is turn on the TV to see couples divorcing left and right fighting over money and other nanny-boo-boo non-sense.

Knowing that little pearl of information, it became my mission to ensure finances would never cause major stress or sabotage a relationship. Of course, ha, that doesn’t mean money has never caused any stress in my life. But there are SO MANY awesome things you can do to financially-proof your life and make things a whole-heck of a lot easier on yourself.

Related: 9 Hidden Ways to Save Money Shopping on Base at the Commissary and Exchange

Military marriages are challenging enough. The last thing you need is to worry about scraping your pennies together to pay the bills. Once my husband and I were engaged to be married and several years into married life, there are several things that we do to keep our financial house in order:

Sit down. Meet. Set some actual financial goals with your spouse.

Before we were married, my husband and I were both pretty darn comfortable spending our money the way we wanted. During our pre-maritial counseling (which I highly recommend) we created financial goals for our future together.

What did we really want our financial house to look like in 5, 10, 20, and 30 years?

And if we wanted it to look like xyz, how were we going to reach those goals exactly?

It’s one thing to want a log cabin in the rocky mountains and another thing to actually think about how much that would cost and how you could achieve that financial goal.

Live off one income (regardless if there are two).

One thing that we started doing before we were even married was to pretend my income didn’t even exist. All of it went straight to savings for various financial goals. We budgeted down to the penny using only his income.

This is for several reasons:

- Military spouse employment can be a bumpy road. Treating your income as savings can save you stress when unemployment hits.

- It helps you reach greater financial goals in a shorter period of time when you are saving an entire income.

Pay off all your bills on time (including the full balance on all credit cards).

You are probably nodding yes, already knowing that this is common information. But I can’t tell you how many people I know racking up credit card debt, late fees, and other unnecessary bills.

Paying your bills on time, and if you choose to use credit cards, always paying off the balance in-full each month will save you thousands, if not more, in the long run.

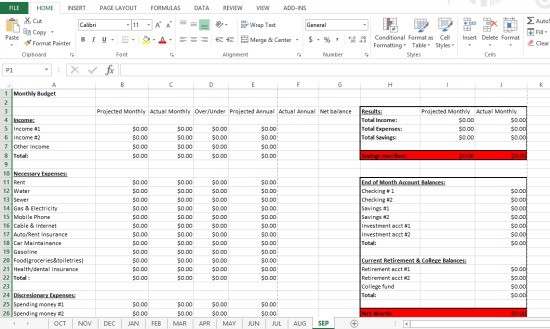

Create a monthly budget and stick to it.

Together we created a spreadsheet and itemized all of our necessary expenses, as well as incidental expenses. You can download my free excel spreadsheet here to Google docs for yourself to use. (Simply open the link, then download and save to your computer. You should then be able to modify and edit the excel spreadsheet. )

Seeing how monthly income breaks down month after month can work wonders when it comes to sticking to a financial plan.

The kicker?

When my husband saw how much our savings was growing each month on the spreadsheet, it helped him become even more committed to our future financial goals.

Hold monthly budget meetings to stay on the same page.

Financial transparency is huge, huge, huge. Did you stick to the budget? Where did you fall short? Be open and honest with each other. Monthly meetings will help you stay on track and make adjustments with the budget.

Have a monthly cash spending allowance.

One major way to cut back on spending is simply to have a “no questions asked” monthly cash allowance. My husband got $100 cash and I got $100 cash. We both used the money to buy unnecessary things that we really wanted.

Lunch out with a friend, a pedicure, a new pair of shoes when I already had 15, a special item off Amazon, etc. You make the rules for the cash allowance, but it’s an awesome way to still feel like you have freedom to spend some money without going overboard.

Create an emergency fund.

Creating an emergency fund is the cornerstone of financially-proofing your life. When things come up you will easily be able to pay for it using your emergency fund. It’s recommended to have approximately 6 months’ worth of living expenses in your emergency fund.

Sounds like a lot of money!

And it is!

But that is what will really save you when the car breaks down, you lose your job, the house incurs major damage, etc.

Invest in Roth IRAs for both spouses, even if one isn’t working.

It’s easy not to think about how you will live month to month once you are both retired. You might be counting on a military pension to support you and your husband in the future, but it’s far from a guarantee.

On top of that, it’s definitely not a guarantee that the pension will be enough to support you both through retirement.

Investing in Roth IRAs is the most tax efficient way to privately save for retirement. We both have accounts through Vanguard.com. It’s easy to set up and their target date retirement funds, make investing extremely inexpensive and incredibly simple for even the most amateur investor.

Another great option to consider is USAA.com. I personally haven’t worked with them, but I’ve heard several testimonies from friends about their amazing customer service and financial options for military families.

Invest in a college 529 plan for the kids.

Did you know that in 20 years it will cost a college-bound student approximately 250,000 dollars to complete a 4 year degree at a public university? That is insane!! Even if you only wanted to contributed 20% to ONE child’s college education that would be 50,000 dollars.

You can choose a state 529 college investment plan for any state that you want—even if you don’t live there! There are a few states that have their 529 plans really nicely put together. We chose the Iowa 529. It’s one of the best in the nation.

They are connected through vanguard.com and again have really nice target date index funds that minimize expenses and make investing very simple. You don’t get the state tax deduction if you don’t live there or file taxes in that state, but for us, the benefits outweighed that factor by far.

One of the other benefits of the Iowa 529 is that other family members can make a donation to the college fund with just a few simple clicks. Also, if one child does not go to college, you can roll it over to another child.

Utilize discounts, freebies and coupons when you can.

Again obvious, but true. If a military discount is offered, don’t be afraid to politely take it.

Minimize, downsize, and keep it that way.

The BEST way to save money is simply not to spend it in the first place. Opting to live in a smaller home, accumulating less stuff, and forgetting about keeping up with the Joneses will save you tens of thousands in the long run and it will help secure your strong financial future.

Great job, Lauren. Good tips.

I usually advise service members to take advantage of the Roth TSP. The fees are even lower than Vanguard’s. Plus your contributions go up with your pay — most service members will get about 7 pay raises in their first 4-5 years.

In the TSP you’re also able to take advantage of special tax treatment for pay earned in a combat zone.

On the other hand, Roth IRAs are a little easier to deal with if you’re going to retire early — that is, quit working altogether before 59 1/2

Thanks, Rob

Yes, great tip. Roth TSP – I haven’t heard of that yet. I will have to take a look. I agree that utilizing the TSP during deployment is a very smart decision. Thanks for your help.

Lauren

Great tips! This information is so important! My husband and I do a lot of these, but I didn’t know about the college savings plans. I definitely want to look into that, especially now before we even have kids.

College is crazy expensive, even if you only want to contribute 25% or less, it is still a pretty large sum of money. We took a big gulp when researching the cost of college for our son. We are saving now to avoid the stress later.